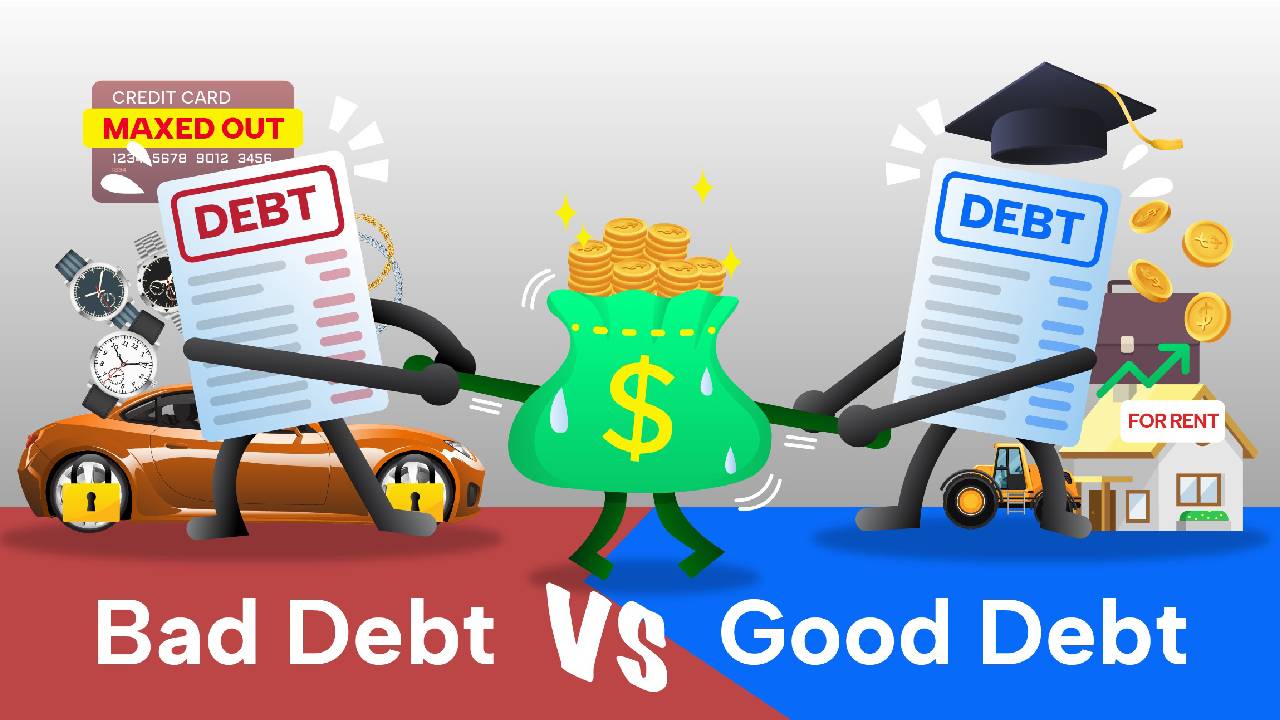

NOT all debt is created equal. Some debt can help build your future, while other types can drag you down financially.

Understanding the difference between good debt and bad debt is essential for making smart money decisions.

Good debt is debt that helps you grow your income or increase your net worth over time. It’s usually tied to an investment in your future.Examples include:

• Student loans – If used wisely, education can lead to better job opportunities and higher lifetime earnings.

• Home loans (mortgages) – Buying a home can build equity and increase in value over time.

• Business loans – If used for a profitable business, this kind of debt can help generate income and create financial independ¬ence.

Good debt often comes with lower interest rates and long re¬payment terms, making it more manageable and beneficial in the long-run.

Bad debt, on the other hand, is money borrowed to buy things that lose value or don’t generate income.

It usually comes with high inter¬est rates and can lead to a debt spiral if not managed carefully. Examples include:

• Credit card debt – Often used for shopping, travel, or dining, with interest rates that can exceed 20 per cent.

• High-interest personal loans – Taken out for non-essential spending or impulse purchas¬es.

• Buy now, pay later schemes – Tempting but often lead to overspending and hidden fees.

Bad debt makes it harder to save and invest and it often leads to stress and financial instability.

If debt helps build your future, it can be good.

If it only funds your present lifestyle and costs you more in the long-run, it’s likely bad.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment