If you’re just loaning a friend a few bucks for lunch, you probably don’t feel the need to write up any kind of formal agreement.

However, if you’re going to be providing your friend with a more substantial loan – such as to open a business, pay off a debt or make a down payment on a car or house – it’s important to put your agreement in writing.

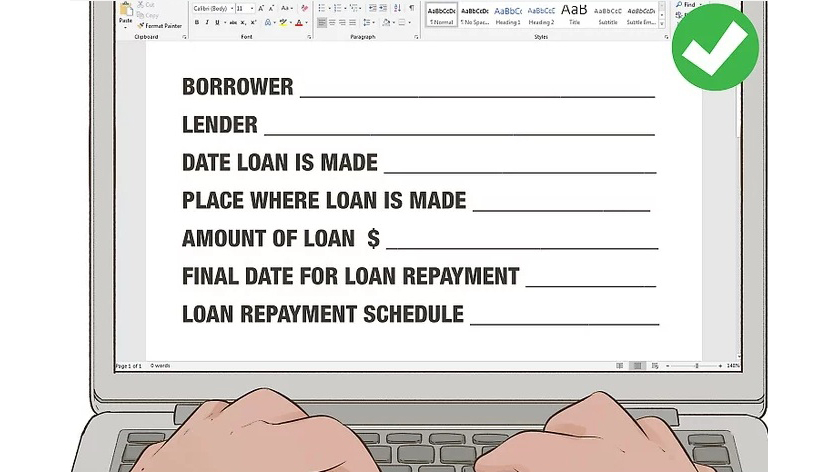

Treating the loan as a business transaction rather than a simple favour may increase the odds that your friend will actually pay you back and ensures the agreement is enforceable in court if problems arise.

Step 1: Meet in person: If possible, meet face to face with your friend to discuss the loan, rather than relying on a phone conversation. Meeting in person allows you both to observe each other’s body language and tone of voice as you discuss various aspects of the loan.

Step 2: Discuss your friend’s financial history and her needs: Before you agree to loan your friend money, make sure you understand why your friend needs the loan and why she’s asking you. Your friend should bring any relevant documents or information along with her, so you can get a sense both of her financial situation and the options available to her.

Step 3: Set an interest rate: Not charging your friend interest on the loan could have tax consequences, depending on the amount you lend. To prove to the IRS that the money is a loan and not a gift, you must charge and collect interest as well as having a formal loan agreement in writing.

Step 4: Decide on a repayment schedule: A solid understanding of your friend’s financial situation will enable both of you to set up a reasonable payment plan that won’t cause a strain. If your friend has had difficulty managing her money in the past, you might consider working with her to develop a budget she can use to control her spending and pay off the loan.

Step 5: Iron out any other issues or conditions: When you make a loan agreement, you want to plan for as many possible outcomes as you can, so brainstorm issues that might come up with your friend and come to an agreement on how that issue will be handled. You should anticipate whether your friend would be able to transfer the loan as well. Suppose your friend becomes severely ill, and her mother offers to take over the payments for her? It probably wouldn’t matter to you who was making the payments, as long as payments were being made, but such a contingency should be spelled out in your agreement.

Step 6: Talk about penalties for late payments: If your friend isn’t able to make payments on time, you may want to include additional fees. Keep in mind that if your friend does have problems making payments later on, the situation can become heated fairly quickly. Creating a plan from the outset when you’re both relatively calm can help you avoid arguments that could happen later if your friend stops paying you and you panic.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment