MBABANE – Women-owned micro, small and medium enterprises (MSMEs) have emerged as one of the most powerful drivers of Eswatini’s economy, yet limited access to finance continues to constrain their growth.

This is according to a comprehensive case study on women’s financial inclusion.

The study shows that women own approximately 60 per cent of all MSMEs in Eswatini, placing them at the centre of employment creation, income generation and household livelihoods. These enterprises are particularly dominant in manufacturing, wholesale and agriculture, sectors that are critical to national food security and economic resilience.

Despite this, the majority of women-led businesses remain informal, small in scale and largely excluded from the formal financial system.

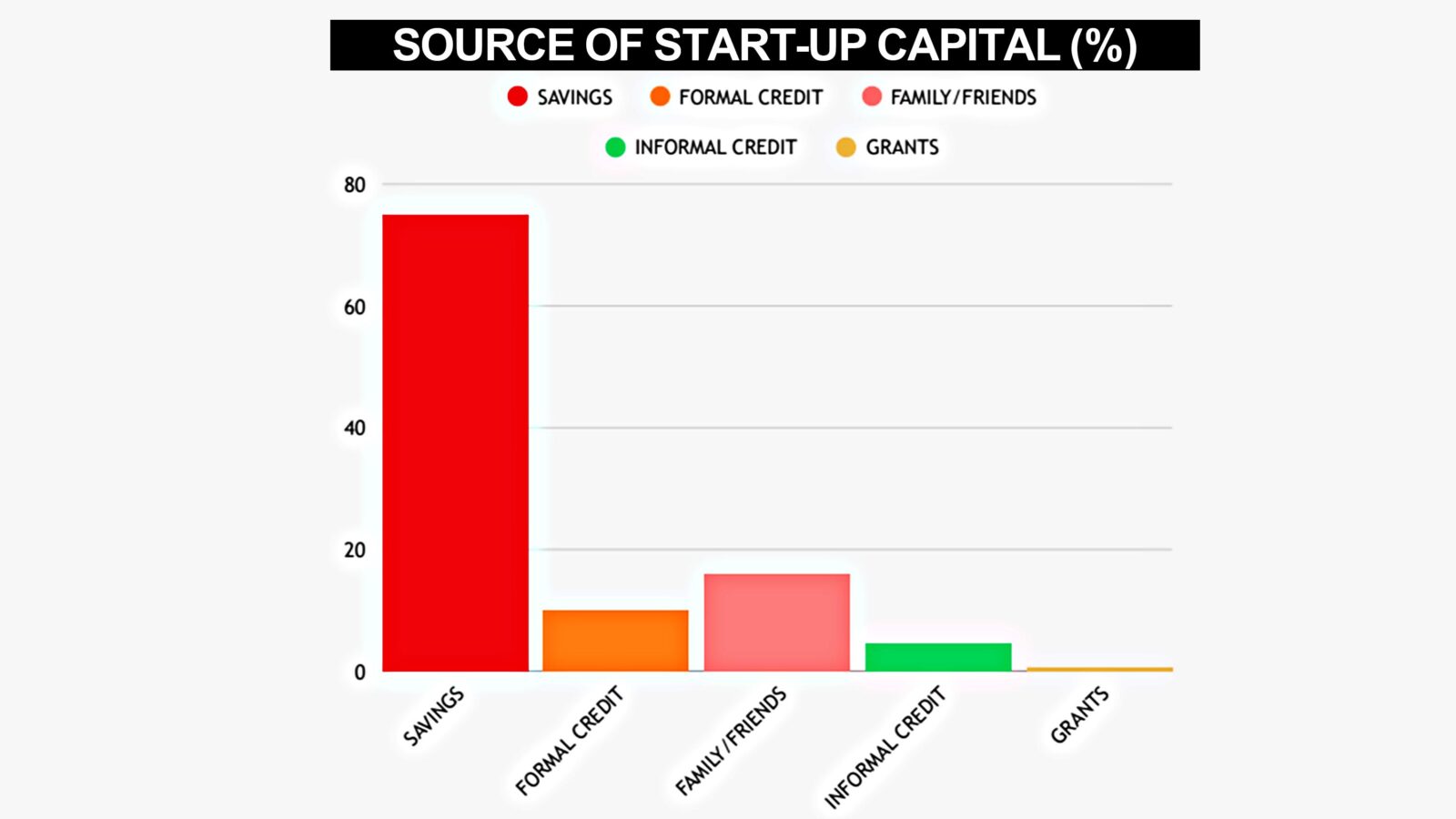

MSMEs are estimated to contribute about 50 per cent to Eswatini’s gross domestic product and employ more than 92 000 people, accounting for roughly 21 per cent of the national workforce. However, the report highlights that only a small fraction of these businesses are able to access formal financing, with nearly 90 per cent relying on personal savings to start or sustain operations.

For women entrepreneurs, the challenge is even more pronounced. In 2024, 74 per cent of firms with a female top manager identified access to finance as their single biggest constraint. This figure reflects deep-rooted structural barriers rather than a lack of entrepreneurial activity or willingness to borrow.

While Eswatini has made progress in improving overall financial inclusion, the report notes a clear disconnect between access to basic financial services and access to growth-oriented finance.

Financial inclusion has risen sharply from 63 per cent in 2011 to 87 per cent in recent years, driven largely by mobile money platforms, no-frills bank accounts and relaxed Know Your Customer requirements. Women are now slightly more financially included than men, particularly in the use of digital financial services.

However, access to credit, insurance and long-term financing remains limited, especially for women operating micro and informal enterprises. The report argues that current financial products and lending models are poorly aligned with the realities of women’s economic lives, which often involve irregular incomes, mixed livelihoods and limited asset ownership.

Land ownership remains one of the most significant barriers. Although Eswatini’s Constitution guarantees equal rights to land ownership, women rarely hold land titles in their own name, largely due to cultural norms and affordability constraints.

This prevents many women from using property as collateral, a key requirement for bank lending. The absence of a movable assets registry further restricts women’s ability to leverage equipment, livestock or inventory to secure financing.

As a result, women-owned MSMEs are disproportionately concentrated in the micro-enterprise category, with 85 per cent operating as sole proprietorships.

These businesses typically employ only one person and are largely survivalist in nature, limiting their capacity to generate broader employment or transition into higher-growth enterprises. Only 27 per cent of women-owned MSMEs are classified as high-growth enterprises, compared to 45 per cent of male-owned businesses.

*…

Access to credit still eludes women

MBABANE – Eswatini’s rapid progress in financial inclusion has positioned the country among regional leaders.

Yet, the benefits of this progress have not translated into meaningful access to credit for women entrepreneurs, according to the case study on women’s MSMEs.

Financial inclusion has expanded over the past decade, with 87 per cent of adults now using at least one formal financial service.

Mobile money platforms, agent banking and no-frills accounts with relaxed KYC requirements have played a central role in bringing women into the financial system. Women are now slightly more financially included than men, particularly in the use of digital payment services. Despite these gains, access to credit remains severely constrained. The report shows that only about 10 per cent of MSMEs are able to secure formal financing, with women-owned enterprises facing the greatest exclusion. For many women entrepreneurs, having a bank or mobile money account do not translate into eligibility for loans, insurance or working capital facilities.

One of the key challenges lies in the design of financial products. Most lending models are built around formal employment, predictable income streams and collateral-based security. However, women’s businesses often operate across multiple activities, combining farming, trading and household responsibilities.

These income patterns are poorly understood by financial institutions, leading to high rejection rates or discouraging women from applying altogether. Collateral requirements further exacerbate the problem.

*…

Rural women remain excluded from formal markets

MBABANE – Rural women play a central role in sustaining Eswatini’s economy, yet remain among the most economically marginalised groups, according to the study on women-owned MSMEs.

Women account for approximately 70 per cent of the agricultural workforce and produce an estimated 90 per cent of the country’s food. Subsistence farming remains a primary livelihood for 75 per cent of the population, with rural women often combining farming with informal trading and small-scale processing to support household income.

Despite their contribution to food security and employment, only 11 per cent of farmers engage in commercial agriculture, reflecting limited access to markets, finance and productive inputs. Women, in particular, face systemic barriers including limited land ownership, lack of collateral and exclusion from formal agricultural value chains.

The report highlights that rural women’s economic activities often fall outside traditional support programmes, which tend to focus either on agriculture or enterprise development, but rarely both. This fragmented approach leaves many women underserved, despite their adaptive strategies to generate income across sectors.

Access to finance remains a critical constraint. Rural women are less likely to have access to bank branches, business development services or formal credit facilities. While mobile money has improved transactional access, it has not addressed the underlying need for investment capital to scale production or enter formal markets.

*Full article available in our publication

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment