The pros

- Lower or no interest. Family and friends might offer loans with little to no interest, making it a cheaper option than a formal personal loan.

- Flexible terms. You’re more likely to get a more flexible repayment schedule with a loved one. For instance, if you lose your job or need to make a late or early repayment, they’ll probably be more accommodating than an official lender.

- Simplified process. Borrowing from a friend or family member doesn’t involve a formal loan application, credit checks and other admin.

- Quick access to funds. The process can be quicker, with no lengthy approval processes involved.

The cons

- Relationship strain. Missing a payment or any kind of dispute can put a strain on the relationship. The best-case scenario is that this makes things awkward for a while, the worst is that it affects your relationship forever.

- You won’t build up your credit history. Borrowing from a friend or family member doesn’t help you build up your credit history like getting an official loan does. This could make it harder to get credit in future.

- Limited borrowing amount. The amount you can borrow is what your loved one can comfortably afford, which might not be enough.

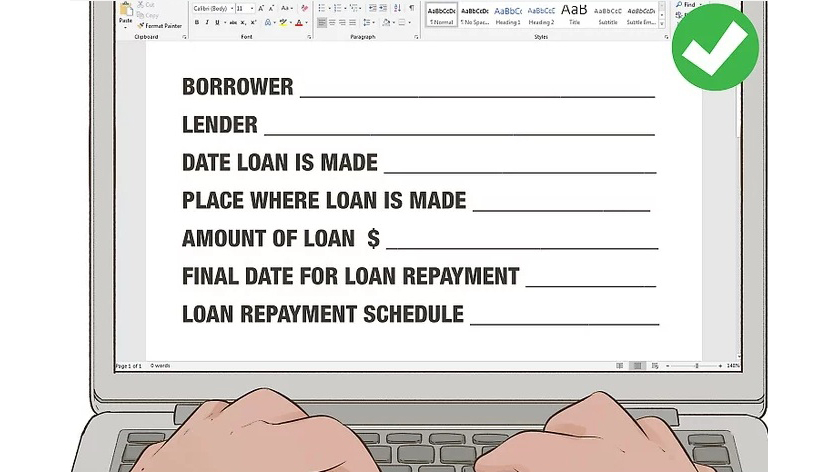

A friendship loan is an act of trust and kindness. To protect both the relationship and your finances, this act must be treated with the same seriousness as a commercial transaction. It’s okay to say no if you’re uncomfortable, and if you say yes, be sure to solidify the terms in writing.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment